Table of Contents

Introduction

The first corporate governance initiative was launched in Hong Kong in the year 1992. The Stock Exchange of Hong Kong (SEHK) was the first body to initiate a Corporate Governance Project in order to promote and further enhance corporate governance standards. In 1993, SEHK established the first Best Practice Code in order to be properly aligned with international developments. Since then, the corporate governance regime has been eventually upgraded in Hong Kong. Prior to conducting a detailed research on the recent improvements witnessed in corporate governance framework in Hong Kong, it is important to understand the significance of corporate governance in real-world scenario. Corporate governance mainly denotes establishing relationship between the management, shareholders, stakeholders and other board members. The concept has gained importance in the past few decades due to various reasons, such as fraudulent activities taking place in the corporate world and East Asian crisis which occurred in late 1990s. Every country, currently, knows the significance of corporate governance in relation to growth and efficiency of domestic economy. It can be stated that good corporate governance leads to proper balance among board members, shareholders and managers. High degree of transparency can be maintained with the help of a proper governance framework. Hong Kong Exchanges and Clearing Limited have been able to update the Code of Practice, since the emergence of Corporate Governance Code in 2005. There are some key practice areas which have been included in the recent years, such as risk management function, governance and environmental reporting, etc. The focus of this research paper will be on the key recent developments in context of Corporate Governance in Hong Kong along with evaluating its fitness-for-purpose in the year 2017.

Research aim and objectives

The main research aim is to analyse the recent developments in the field of corporate governance in Hong Kong. In this research paper, the recent trends will be critically explored which has transformed the code of practice being followed in the region. The main research objectives to be addressed in this particular study are:

- To understand the importance of corporate governance practice

- To analyse the recent developments in corporate governance in Hong Kong

- To evaluate the fitness-for-purpose of the framework in 2017

- To correlate theoretical concepts with information gained about current corporate governance in Hong Kong

Theoretical context

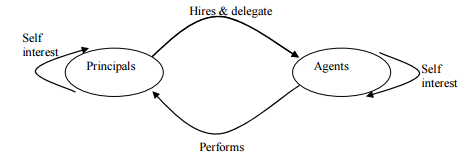

As per Baker and Anderson (2010, pp. 56-57), corporate governance can be stated as a set of structures and processes required for directing and controlling an organisation (Baker and Anderson, 2010). Arguably, the concept is used in case of strategic decision-making process. The effective implementation of undertaken decisions also requires active support of corporate governance framework. Corporate governance involves all forms of firms and even extends to various non-economic and economic activities. There are some fundamental theories which govern the concept of corporate governance, as claimed by Tricker and Tricker (2015, pp. 71-72). According to Aguilera and Jackson (2010, pp. 521-522), the agency theory is a simple framework that symbolises corporations to be a body of two participants, i.e. shareholders and managers. As per this theory, managers or employees within an organisation can even be self-interested. Figure 1 further elaborates the agency model.

Figure 1: The Agency Model

(Source: Lan and Heracleous, 2010)

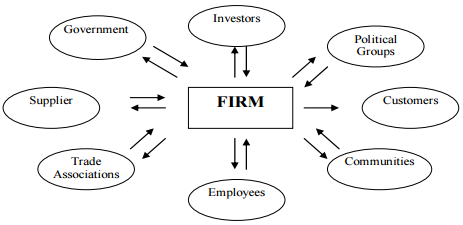

Shareholders usually expect that the agents would undertake sensible decisions in favour of the principal’s interest (Aguilera and Jackson, 2010). Arguably, agents might not make such decisions which are completely aligned with shareholders’ interest. As mentioned by Lan and Heracleous (2010, pp. 300-304), to a certain extent, these problems were somewhat addressed in the agency theory. On the basis of agency theory, it is evident that the agent might be succumbed to opportunistic behaviour, self-interest and even short of congruence between the specific aspirations of the agent’s and principal’s pursuits. The theory was framed so as to differentiate between control and ownership. A relatively more individualistic view is taken into account in this particular model. The theory has been used to explore the relationship between the management structure and ownership. In case of a separation, the agency model is employed so as to align managerial goals with the basic aim of an owner. This theory clearly indicates that employees or people would be definitely accountable for their responsibilities and tasks. Employees should not only be focused on fulfilling needs of shareholders, rather they need to be conscious about setting up a proper governance structure (Lan and Heracleous, 2010). As argued by Lin and Hwang (2010, pp. 62-64), stakeholder theory is one of the most important frameworks in the area of corporate governance. Corporate accountability is greatly involved in this particular framework to provide guidance to wide array of stakeholders (Lin and Hwang, 2010). According to Mason and Simmons (2014, pp. 79-80), the theory contradicts the basic assumption of the agency theory where managers were witnessed to serve desires of shareholders. Stakeholder theory states that organisational managers need to take into consideration network of relationships, comprising of business partners, suppliers and employees (Mason and Simmons, 2014). The group of network has been highlighted in figure 2.

Figure 2: Stakeholder Theory

(Source: Spitzeck and Hansen, 2010)

As argued by Spitzeck and Hansen (2010, pp. 383-384), the theory attempts to outline stakeholders who require attention of the management. The procedure of decision-making is completely based on the relationship network, as demonstrated in the stakeholder theory (Spitzeck and Hansen, 2010).

Several frameworks have developed in Hong Kong’s corporate governance. In the above section two models have already been provided. On one hand, stakeholders’ theory focuses on different relationships that take place with many groups in respect to individual benefits; on the other hand, resource dependency theory emphasises on board of directors’ role pertaining to resources required by different firms as state by Lin, Liu and Zhang (2016, pp. 91-118). Directors play important role in any firm’s resources. The directors are also important in securing or providing essential resources to a company via linkages to the outside environment. It mainly focuses on independent organisations’ appointment of representatives. They are appointed in order to gain access in firm’s success level related to resources. For instance, if the outside or independent directors are by any chance partnered with any law firm then he or she can definitely provide any legal help to the company during financial crisis. The help can be rendered in two different ways such as private communication and board meetings with the firms’ executives. It can be inferred that if the firm had to access legal help from outside sources then the same would prove to be more cost incurring as mentioned by Bae, Baek, Kang and Liu (2012, pp.412-435). In fact, it is also argued at times that organisational functions are enhanced by provision of resources. Directors definitely contribute to the firms’ resources such as skills, information, access to any key constituents, etc; these constituents include buyers, suppliers, social groups, public policy makers and legitimacy. On the other hand, directors can be categorised into four main types; they are namely, business experts, insiders, support specialists as well as community influencers. Insiders are former and current executives working in the firm to provide various expertise advices in specific areas; these areas include laws and finances of the firms. Business experts are mostly former senior executives, current executives and others. Masulis, Wang and Xie (2012, pp.527-554) on the other hand, support specialists are bankers, lawyers, public relations experts, insurance company representatives, etc. They provide robust support in individual specialised field. Lastly, the community influencers are said to be leaders of the community or social organisations, members of clergy, university faculty, political leaders, etc.

Analysis and Findings

The Hong Kong Exchanges and Clearing Limited (the Exchange) has brought forth significant changes into the existing Code of Practice. The series of changes have been incorporated into different fields of practice. It is evident that the Code has been updated so as to be properly aligned with the international standards of practice. The changes introduced are inclined towards risk management function, enhancing accountability of the management and the board, and further strengthening guidelines for governance, environmental and social reporting. Risk management and internal control can be denoted as a key area of concern for real-world organisations (Thomson Reuters, 2016). This particular title has been amended in the existing code of practice. The conditions related to risk management has been added so that required measures are undertaken in desirable time-frame. According to the new improvements, the management need to provide confirmation to all board members in relation to effectiveness of the internal control systems and risk management procedure (Claessens and Yurtoglu, 2013). The changes have been extended to the Internal Audit as well. It is essential for the issuers to consider the internal audit function. It has also been defined that the stated function can either be outsourced or in-house. The annual review conducted by the board would reflect upon resource adequacy, staff experience and qualifications, budget set for the internal audit function of the issuer and distinct training programmes. A new principle has also been enforced upon the audit committees where members can include risk management practices as and when required. In terms of reference, the audit committee should involve review of financial controls of issuer (Fung, 2014). It can be claimed that the recent improvements in corporate governance in Hong Kong decreases the dependency level of audit committee on the board or the board risk committee to a certain level. For instance, the recent developments facilitate the audit committee to closely scrutinise the issuer’s internal control systems and risk management mechanism.

In the current corporate governance framework, there are various subject areas included which were previously not given much importance. The current approach requires the board to consistently review the issuer’s internal control systems and risk management mechanism, rather than focusing only on one-time review. There are additional responsibilities which are assigned to board members so as to ensure that the network of relationships, as defined in the Stakeholder Model, is properly maintained (Kim and Lu, 2013). The annual review of the board needs to consider quality and scope of on-going monitoring of internal control systems and risks, communication frequency of monitored results, significant changes since the last review session, identified control weaknesses and effectiveness of the process undertaken by the issuer for Listing Rule compliance and financial reporting. It is important for issuers to disclose relevant information related to disseminating and handling of inside information. On the other hand, the compliance statement even include disclosure of a narrative statement by issuers on the degree to which they have been in line with the internal control code and risk management provisions during the mentioned time-frame (Law, 2011). Arguably, there are some areas which have still not been addressed within the corporate governance framework in Hong Kong. In 2017, the fitness objective will be accomplished only when the multi-dimensional perspective is taken into account.

The aspect of fitness-for-purpose will hold relevance only when the framed changes initiated since January 2017 follows the necessary schedule. As claimed in the Stakeholder theory, role of managers is not only confined to limited number of stakeholders, rather wide array of relationships need to be maintained. For instance, fair treatment of all policy holders is an important factor covered in the current corporate governance framework. The fair treatment policy is fit enough for the current business trends in Hong Kong (PWC, 2015). It shall help in meeting legitimate interests of all stakeholders. Guidance Note (“GN”) 10 basically sets out the standards of corporate governance to be met. GN 10 is not only appropriate for 2017 but also future years to come. The changes introduced consider policy holders’ interests to be a regulatory issue as well as a business issue. It can be argued that with each passing year, competitive rivalry of the marketplace is increasing (Cheung et al., 2011). Hence, in the current financial year, increased rate of competition has also triggered various technical issues, such as cyber security problems. Arguably, the new corporate governance standards introduced in Hong Kong is closely inter-linked with such marketplace issues (Arner et al., 2016). Therefore, the set standards are definitely fit-for-purpose, as of the current financial year. Cyber security policy has been made the core of business operations where accountability of the management is increased in relation to mitigating, preventing, detecting and identifying various cyber security threats.

The listed companies should only follow existing CG codes. In fact, these companies are actually bound by the same. On the contrary, privately owned limited companies are hardly listed in the CG code. Several listed companies were actually incorporated out of Hong Kong’s jurisdiction. As a result, part 16 is only applicable in case of non-Hong Kong companies. All these companies’ main place of operating is Hong Kong though. The board of directors apart from the organisations itself are bound by codes of CG (Khan, Muttakin and Siddiqui, 2013). The codes are instrumental in verifying and ensuring compliances with various listed companies. In case of frauds the board of directors may actually get involved in any criminal liability case or attract civil liabilities as well under laws and regulations of Hong Kong. Statutory backing is required for corporate governance or else its application cannot be appropriate (Kathy Rao, Tilt and Lester, 2012). Both the crisis of 2008 and 2004 have portrayed why corporate governance and its application is required. 80 percent investors are actually ready to pay premium for the companies that matter for them the most. Real challenges have already been identified previously in case of embedment of adequate details for principles of corporate governance. The detail may not be taken into consideration by the local legislations (Michelon and Parbonetti, 2012). Fundamental requirements such as transparency, certainty, clear articulation, enforceability, independence, responsibilities and accountability may not be fulfilled if statutory essentials do not back up the corporate governance. However, several hurdles have been faced for bringing statutory backings into corporate governance. Self-regulation is actually nothing new in case of company affairs’ supervision. It is more flexible or cheaper way of problem-solving. Substantial drawbacks are there for self-regulatory reliance, especially when all the market participants are hardly self-disciplined.

Summary of key issues and potential actions/changes

The potential changes in the corporate governance in Hong Kong are centred towards bringing forth overall organisational development. There are some changes which have come into effect from January 2017. It is evident that the potential changes are mostly inclined towards upgrading expertise level of board members, establishing fair treatment policy for all stakeholders, defining role of the Chief Executive and Chairman, scheduling of committee reviews, and provision of non-executive director within the audit committee and inclusion of business continuity policy (Arner, Hsu and Da Roza, 2010). All of these changes reflect the significance of the Stakeholder Theory in real-time business operations. It has been revealed that these changes are the first phase of change, the second phase of change is to be introduced in 2018 in Hong Kong. In the nearby future, the suggested changes are in context of establishing standalone risk committees. An effective corporate governance framework will be established when the risk committee is separate from the audit committee (Yu and Rudge, 2014). Terms of reference for the individual committees need to be established for securing better results. It would be easier for a separate risk committee to identify distinct flaws within the existing business system.

Hong Kong’s corporate governance has topped the list. The survey conducted on corporate governance has been conducted on institutional investors and fund managers in order to give scores related to corporate governance culture, auditing and accounting, regulatory and enforcement environment as well as corporate governance rules (Man and Wong, 2013). Hong Kong Institute of accountants certified public reports for regulating various firms and their corporate governance. However, the government actually wants to give the responsibility to Financial Reporting Council entirely so that all the firms abide by the rules and regulations of corporate governance. For instance, two issues can be witnessed vividly in case of Hong Kong. One is that the women hardly get position in board of directors. As a result, they are always devoid of becoming C-level managers. It can also portray broader societal issue. Gender discrimination can be thus witnessed when women are not chosen for those positions. On the contrary, another issue identified was lack of proper audit committee. Audit committee is necessary because without their interference it is not possible to properly monitor all the internal audit working. Moreover, they can also look after the company’s compliance and fairness with the financial statements (Adams, 2012). Sometimes when the companies are devoid of audit commit it becomes difficult to understand whether the financial statements are appropriately prepared or not. As a result, both these issues need more concentration for better performance of the companies in Hong Kong. Even though there are several intelligent workmen in Hong Kong, they are not given scope.

Conclusions & Recommendations

The above research paper has portrayed the various reforms taken place in Hong Kong in relation to corporate governance. Since the last few years, there are consistent changes being made in corporate governance. It is a common assumption that corporate governance sets forth a framework for facilitating interaction between management and shareholders. However, this research paper has been able to reveal the significance of corporate governance in various fields. In Hong Kong, the amended changes in corporate governance are mostly centred towards distinct control functions, internal audit, intermediary management, risk management and compliance. The study has well demonstrated the key developments and potential changes to be undertaken in the coming years. As highlighted in the research paper, the main issue with corporate governance is lack of an independent auditor’s committee. It is highly recommended that the internal audit committee should be separate from the risk management committee. A wider array of responsibilities can be effectively undertaken if both the committees can be easily differentiated from one another. On the other hand, the corporate governance reform does not lay emphasis on women empowerment. Hence, it is essential that number of women on board should be increased. Better investment decisions can be undertaken if there is more focus on transparency and reduced discrepancy.

- Adams, R.B., 2012. Governance and the financial crisis.International Review of Finance, 12(1),7-38.

- Aguilera, R.V. and Jackson, G., 2010. Comparative and international corporate governance. Academy Of Management Annals, 4(1), pp.485-556.

- Arner, D., Hsu, B.F. and Da Roza, A.M., 2010. Financial regulation in Hong Kong: Time for a change. Asian Journal of Comparative Law, 5(1), pp.1-47.

- Arner, D.W., Hsu, F.C.B., Goo, S.H., Johnstone, S. and Lejot, P.L., 2016. Financial markets in Hong Kong: Law and practice. Oxford: Oxford University Press.

- Bae, K.H., Baek, J.S., Kang, J.K. and Liu, W.L., 2012. Do controlling shareholders’ expropriation incentives imply a link between corporate governance and firm value? Theory and evidence.Journal of Financial Economics, 105(2), pp.412-435.

- Baker, H.K. and Anderson, R. eds., 2010. Corporate governance: A synthesis of theory, research, and practice. New Jersey: John Wiley & Sons.

- Cheung, Y.L., Connelly, J.T., Jiang, P. and Limpaphayom, P., 2011. Does corporate governance predict future performance? Evidence from Hong Kong. Financial Management, 40(1), pp.159-197.

- Claessens, S. and Yurtoglu, B.B., 2013. Corporate governance in emerging markets: A survey. Emerging Markets Review, 15, pp.1-33.

- Fung, S., 2014. Hong Kong auditing: Economic theory & practice. Shanghai: City University of HK Press.

- Kathy Rao, K., Tilt, C.A. and Lester, L.H., 2012. Corporate governance and environmental reporting: an Australian study.Corporate Governance: The International Journal of Business in Society, 12(2), pp.143-163.

- Khan, A., Muttakin, M.B. and Siddiqui, J., 2013. Corporate governance and corporate social responsibility disclosures: Evidence from an emerging economy.Journal of Business Ethics, 114(2),207-223.

- Kim, E.H. and Lu, Y., 2013. Corporate governance reforms around the world and cross-border acquisitions. Journal of Corporate Finance, 22, pp.236-253.

- Lan, L.L. and Heracleous, L., 2010. Rethinking agency theory: The view from law. Academy of Management Review, 35(2), pp.294-314.

- Law, P., 2011. Audit regulatory reform with a refined stakeholder model to enhance corporate governance: Hong Kong evidence. Corporate Governance: The International Journal Of Business In Society, 11(2), pp.123-135.

- Lin, J.W. and Hwang, M.I., 2010. Audit quality, corporate governance, and earnings management: A meta‐International Journal of Auditing, 14(1), pp.57-77.

- Lin, Z.J., Liu, M. and Zhang, X., 2016. The Development of Corporate Governance in China.Asia-Pacific Management Accounting Journal, 1(1), 91-118.

- Man, C.K. and Wong, B., 2013. Corporate governance and earnings management: A survey.Journal of Applied Business Research, 29(2), pp.391-400.

- Mason, C. and Simmons, J., 2014. Embedding corporate social responsibility in corporate governance: A stakeholder systems approach. Journal of Business Ethics, 119(1), pp.77-86.

- Masulis, R.W., Wang, C. and Xie, F., 2012. Globalizing the boardroom—The effects of foreign directors on corporate governance and firm performance.Journal of Accounting and Economics, 53(3),527-554.

- Michelon, G. and Parbonetti, A., 2012. The effect of corporate governance on sustainability disclosure.Journal of Management & Governance, 16(3),477-509.

- 2015. Corporate governance code and corporate governance report – What are the key changes? [Online] Available at: <http://pwccn.com/webmedia/doc/635663301288848086_ra_corp_gov_code_jan2015.pdf> [Accessed 11 February 2017].

- Spitzeck, H. and Hansen, E.G., 2010. Stakeholder governance: How stakeholders influence corporate decision making. Corporate Governance: The International Journal Of Business In Society, 10(4), pp.378-391.

- Thomson Reuters. 2016. Upcoming changes to Hong Kong’s corporate governance framework for insurers. [Online] Available at: http://www.hk-<lawyer.org/content/upcoming-changes-hong-kong%E2%80%99s-corporate-governance-framework-insurers> [Accessed 11 February 2017].

- Tricker, R.B. and Tricker, R.I., 2015. Corporate governance: Principles, policies, and practices. Oxford: Oxford University Press.

- Yu, B. and Rudge, L., 2014. Hong Kong corporate governance: A practical guide. [Online] Available at: <http://www.hkcg2014.com/pdf/hong-kong-corporate-governance-a-practical-guide.pdf> [Accessed 11 February 2017].