Table of Contents

Introduction

Sierra Ltd specializes in manufacturing and selling of automotive parts required in luxury cars. The company is partly owned by the founding members of Sierra family and there is also considerable long term debt in the book of accounts. The main concern of the lenders and shareholders is declining profitability in recent years. The manager of boutique management consultancy, William Kan, visited one of the companies of Sierra Ltd, and collected some financial data including notes of management meeting. The findings highlight that the company is currently facing some issues with current management accounting practices. As an expert in the field of costing, pricing and management accounting practices, I will address the current issues in this report by assessing the current costing and pricing practices of Sierra Ltd and then recommend whether or not activity based costing (or ABC) suitable for the firm. This report will also assess the major factors that the management team should consider should it consider to accept the proposal.

Current costing and pricing practices of Sierra Ltd

The finance director at Sierra Ltd, Baljit Kaur, made some important observations regarding the current costing and pricing practices of the company which was highlighted in the recent management meeting. The problem with traditional product costing is the overhead allocation associated with direct materials and labour cost. It is easy for the company to trace direct expenses associated with various product lines but in highly automated business machine hours are considered as basis for allocation of production overheads. This assumption distorts some of the product costs which can be explained with the following example:

The transmission components product line manufactured by the company has multiple variants specific to the varying needs of the customers. As a result, there is need to adapt separate production line for every variant. This makes the production process very complex requiring lot of labour hours and time for manufacturing. In contrast, the clutch and engine components have less number of variants which simplifies the manufacturing process (as less number of parts will be assembled). This helps to standardise products having long production lines with limited set ups. In general, the company adds a 30% margin to full manufacturing costs (considering all product lines) to arrive at sales price. However, Baljit argues that there is a chance that this costing and pricing strategy will fail to cover the non-production overhead costs of the company. As a result, the company will not be able to make adequate profit margins and will affect the market competitiveness adversely. Hence, the finance director of the company suggests that instead of using traditional basis for product costing, Sierra Ltd should upgrade the current accounting system to incorporate activity based costing.

The sales director, Chris Singleton, also expressed concerns because even the small start-up firms are using agile product design and development process. However, most of these companies specialise in one product line having few variants. This makes the production process less complex and the traditional product costing is suitable in these cases as they have relatively low overheads. It facilitates these companies to retain competitive advantage by reducing product pricing. Chris agrees with Baljit and suggests that if the product prices are not lowered then both sales revenues and market share would likely fall in future.

The other members of the management team, namely Silvia Sierra (Managing Director at Sierra Ltd) and Mathew Capri (Production Director) have slightly different views on the issue. As per the arguments of Silvia, the current costing system has been serving adequately over the past decade or so. The company has also invested lot of time and resources in training the accounting staff to understand the use of software. If the current accounting system is updated to activity based costing then it will make the implementation process very expensive in terms of annual data collection and training for use of new software. It was further noted by Silvia that there was a need to lower the production cost of engine components because this product line have conventionally contributed almost 50% of total revenues. In contrast, the contribution of transmission and clutch components have been stable which does require additional investment. The production director is also apparently not comfortable with untested accounting system change. Hence, there is a need to justify the need for accounting system change with appropriate evidences.

Suitability of Activity Based Costing (or ABC) for Sierra Ltd

According to Mahal and Hossain (2015), the implementation of activity based costing is often considered as a daunting activity because it involves the tedious task of data accumulation but once implemented it can help to improve financial results by streamlining focus on key areas. The major areas that the management of Sierra Ltd will have to consider are:

- Strategic level analysis – According to CIMA (2008), if the management wants to conduct a top level analysis then activity based costing should be implemented across all product lines to reflect a comprehensive view of production units. On the other hand, the main issue of the organisation is strategic cost management which requires the management to streamline implementation to individual tasks.

- Focusing on specific areas – As per the arguments of Silvia, Managing Director, there is a need to reduce the cost of production for the engine components. Activity based costing will allow the company to focus on the operations of this product line. According to Duh et al (2009), activity costing focusing on specific areas also improves credibility of the process by producing meaningful and comprehensive information.

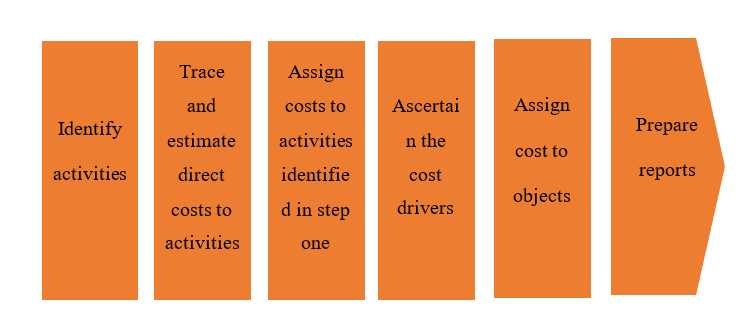

Figure 1: Process of activity based costing

(Source: Author’s creation)

The above figure explains the process of activity based costing and indicates that it gives special attention to cost drivers that influences product costs to increase. According to Drury (2015), the traditional product based accounting used by Sierra Ltd tends to focus more on volume-related drivers like labour hours. However, by implementing the activity based costing it will be possible for the organisation to focus on transaction-based drivers. This will assist Sierra Ltd to consider non-production overhead costs which is traditionally viewed as fixed costs under traditional system. This method will provide more accurate estimates of engine components product line and ultimately leading to more precise pricing decisions.

As per the arguments of Major and Hopper (2005), activity based costing will help the management of Sierra Ltd to increase the understanding of basic cost drivers and overheads. This will allow the managers to control or even eliminate overhead costs.

Advantages of implementing the new accounting system

According to Zimmerman and Yahya-Zadeh (2011), activity based costing will allow the firm to assign production overhead costs more appropriately to respective products compared to traditional accounting approach that simply allocates costs on the basis of machine hours.

- Identifying costs – As per the arguments of the finance director and sales director, Sierra Ltd will have to lower the cost of production which will help to lower prices of goods and increase competitive advantage over rival firms. Activity based costing allows identification of overheads and costs related to production process (Macintosh and Quattrone, 2010).

- Measurement of activity drivers – The data collected by the new system will allow the management to gather information regarding the main drivers and allocate costs accordingly (Naidoo, 2002; Porteus, 2001).

- Assign costs – The process assigns cost to only those activities whose products are in demand. For example, it was mentioned in the management reports that the transmission component is a high volume product with multiple variants whereas the engine component is less complex and requires lower setups. On the basis of current practices, the accountant will allocate all of its overhead costs to products on the basis of machine hours and then add 30% margin. However, this process will not cover the non-production overhead costs to make adequate profits (Porteus, 2001). This means that the company will not be able to reduce prices and if they forcefully reduce prices profit margins will shrink further. In contrast, the activity based costing will help the company to identify the cost drivers and allocate costs more accurately. In this example, the system calculate the cost of all resources used in production but allocate costs only to the products activities which have high demand (Kaplan and Anderson, 2013).

Important factors to be considered by the management team

The implementation of activity based costing will be successful only if the following factors are considered by the management of Sierra Ltd:

- Training requirements – There is a need to conduct workshop sessions for accounting staff and senior management so the concept of activity costing is clearly understood (Garrison et al, 2010).

- Defining scope – Sierra Ltd should define the scope of project in line with organisation’s objectives (Garrison et al, 2010).

- Identify the drivers – The new system should accurately ascertain the drivers of costs.

- Software integration – Incorporating activity based costing in the business process will require system upgradation, data validation and reconciliation (Baldvinsdottir, Mitchell and Nørreklit, 2010).

- Interpretation – The new system should prepare detailed management reports assisting in efficient pricing-decisions and assist in developing competitive advantage in the market over rival firms (Cinquini and Tenucci, 2010).

Summary

As already discussed in this report the main points are summarised below:

It is easy to trace direct costs (production overheads) to respective products but it is more difficult to accurately ascertain and allocate indirect costs to products. The most important consideration is the identification of cost drivers which is influences the cost of activity. For example, as per the arguments of Mahal and Hossain (2015), the main driver of engine components are likely to be machine operating hours which drives maintenance, labour and overheads during activities. Therefore, by implementing the activity based costing Sierra Ltd will be able to evaluate the cost of elements of entire product lines. This will help to identify and control overpriced products (in this case the cost of engine components that has traditionally accounted over half of company’s revenues). Hence, the findings of this report agrees with the literature of Shields (1995) and states that activity based costing should replace the existing product based accounting system.

Recommendations

The management of Sierra Ltd should consider activity based costing system as per the recommendations of the finance director because the new management accounting system will allow them to take pricing decisions more accurately by focusing on both production and non-production overheads. The new system will prevent distortion of some product costs which is frequent in the highly automated business and improve profit margins. Efficient costing and pricing decisions will help the organisation to increase competitive advantage by relatively lowering their product prices and increase market share.

- Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory and practice in management accounting. Management Accounting Research, 21(2), pp.79-82.

- CIMA, 2008. CIMA topic gateway series number 1: activity based costing. [pdf] Available at: < http://www.cimaglobal.com/Documents/ImportedDocuments/cid_tg_activity_based_costing_nov08.pdf.pdf > [Accessed 07 January 2017]

- Cinquini, L. and Tenucci, A., 2010. Strategic management accounting and business strategy: a loose coupling? Journal of Accounting & organizational change, 6(2), pp.228-259.

- Drury, C., 2015. Management and cost accounting, 9th edition. Boston: Cengage Learning.

- Duh, R.R, Lin, T.W., Wang, W.Y., and Huang, C.H., 2009. The design and implementation of activity based costing: a case study of a Taiwanese textile company. International Journal of Accounting and Information Management, 17(1), pp. 27-52.

- Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., 2010. Managerial accounting. Issues in Accounting Education, 25(4), pp.792-793.

- Kaplan, R. and Anderson, S.R., 2013. Time-driven activity-based costing: a simpler and more powerful path to higher profits. Brighton, Massachusetts: Harvard business press.

- Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An organizational and sociological approach. New Jersey: John Wiley & Sons.

- Mahal, I. and Hossain, A., 2015. Activity-Based Costing (ABC)–An Effective Tool for Better Management. Research Journal of Finance and Accounting, 6(4), pp.66-73.

- Major, M. and Hopper, T., 2005. Managers divided: Implementing ABC in a Portuguese telecommunications company. Management Accounting Research, 16(2), pp.205-229.

- Naidoo, S., 2002. Voyage of discovery. Financial Management, 1(1), pp. 32-33.

- Porteus, J., 2001. As easy as ABC. Financial Management, 1(1), pp. 40-41.

- Shields, M.D., 1995. An empirical analysis of firms’ implementation experience with activity-based costing, Journal of Management Accounting Research, 7(1), 148-166.

- Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and control. Issues in Accounting Education, 26(1), pp.258-259.